- Big mistake: Quitting right before a vesting or payout milestone can erase real money because eligibility is based on calendar status, not effort.

- Four buckets: Check Retirement match vesting, RSUs or performance shares, Stock options exercise windows, Bonus or commission payout rules.

- Date rules: Confirm how your company defines “last day” and what counts as employed on a vest date, because “close enough” usually fails.

- Decision framework: Choose to Wait, Negotiate, or Walk by quantifying what you forfeit and comparing it to the cost of staying.

- 48-hour checklist: Verify vesting percentages, next vest dates, option deadlines, and payout eligibility in writing before you click “send.”

Don’t Quit One Week Before Your Payday

The most expensive resignation mistake isn’t emotional. It’s administrative. People hit “send,” feel relief, and then realize their vesting period stock options were scheduled to vest next week. Your manager won’t stop you, payroll won’t warn you, and your equity portal won’t flash an “are you sure?” screen – because vesting is a calendar, and calendars don’t care how done you feel.

Here’s the pattern: you plan to quit on a Friday, and your next vest date is the following Monday. You assume “close enough” counts. It usually doesn’t. Many plans treat your last working day (or your last day of employment) as the end of eligibility, and that tiny date mismatch is where real money disappears. This guide is about one thing: making sure your exit timing is a decision you chose, not a paperwork accident.

The Four Money Buckets That Hide in Plain Sight

Before you resign, do a quick inventory. Most “I lost money when I quit” stories come from the same four buckets. You don’t need to become an expert in equity compensation – you just need the dates and the rules in writing. Once you have them, the resignation becomes a strategy problem, not a mood.

- Retirement match vesting (your employer’s match may not be fully yours yet)

- RSUs or performance shares (shares that vest on specific dates)

- Stock options (your right to buy shares later – often with a post-exit deadline)

- Bonus or commission timing (policies and payout dates can be stricter than you expect)

How Vesting Really Works When You Leave

Vesting rules feel unfair because they don’t reward effort – they reward status on a date. In practice, plans usually ask one blunt question: “Were you eligible on the vesting date?” If the answer is no, the system doesn’t negotiate. That’s why “I worked for it” and “I was basically there” rarely matter once the termination is processed.

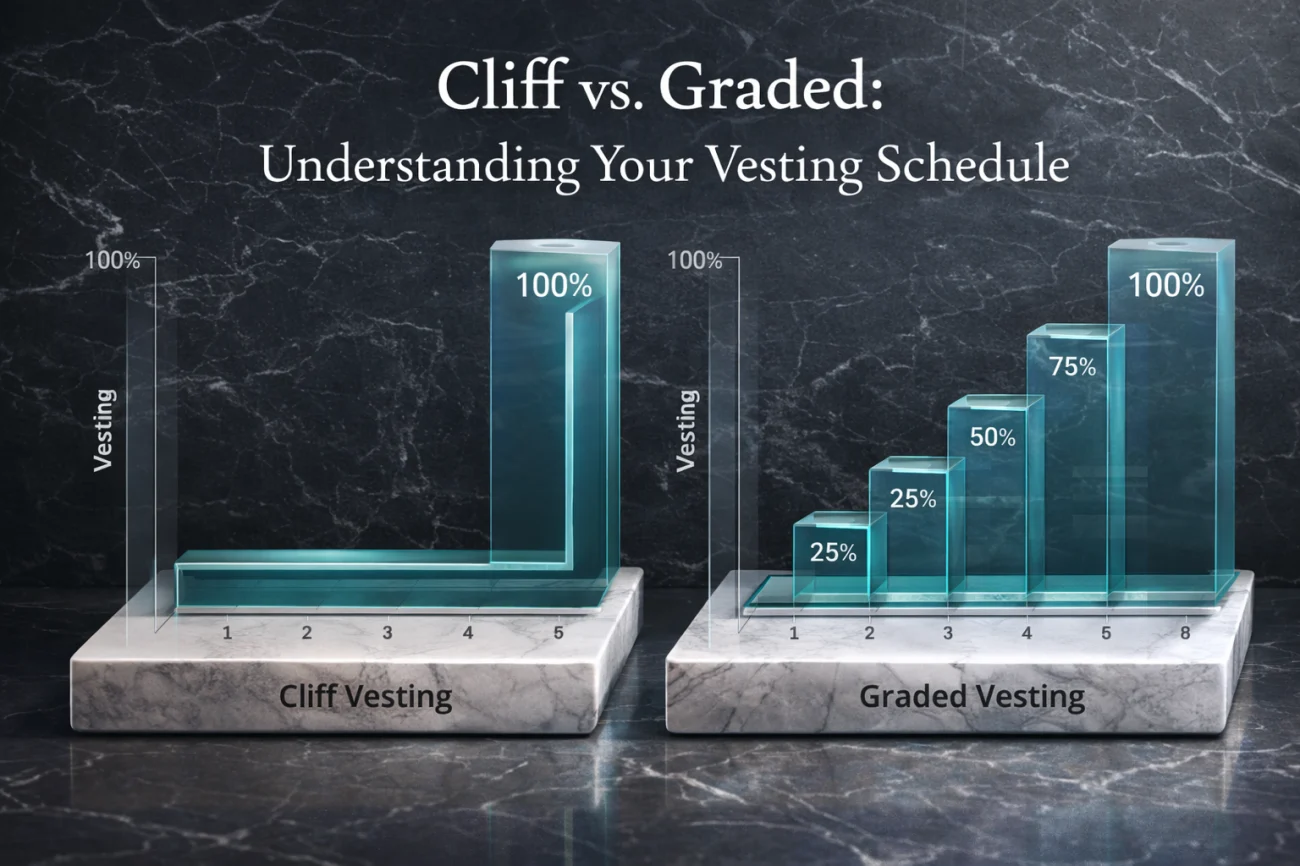

Two details matter more than people expect. First, whether your plan uses cliff vesting (nothing until a milestone, then a big chunk) or graded vesting (small portions vest over time). Second, how your company defines your “last day.” Some organizations treat your last working day as your separation date. Others treat the end of your notice period as your separation date. You can’t safely assume which one you’re in unless you confirm it.

The Quiet Rule People Forget: Your Retirement Match

A lot of people assume their retirement account is fully theirs because it’s in their name. Your contributions usually are. The employer match is where surprises happen. If your plan has 401k vesting rules, the match may vest gradually (or all at once) after a tenure milestone, and leaving before that milestone can mean forfeiting part of the match – even if the dollars have been sitting in the account for months.

The fast check is simple: open your retirement portal and look for “vested balance” versus “total balance.” If there’s a gap, that gap is the money at risk. Then confirm (in writing if possible) your vesting percentage today and your next vesting milestone date. If you’re close, you’ve just turned resignation timing into a calendar decision you can control.

RSUs and the “Close Enough” Myth

RSUs feel like a promise, but they’re a scheduled event. The vest date is the gate. If you leave a day early, most plans treat it the same as leaving a year early. That’s why the safest question isn’t “When do my shares vest?” It’s “What qualifies as employed on the vest date?”

When you’re thinking about rsus when quitting, focus on three things: your next two vest dates, the share count at each date, and the plan language for eligibility. Some plans require active employment through the end of the vesting day. Others apply different rules depending on whether you resign, get laid off, or are terminated. Don’t rely on hallway wisdom. Get the plan summary, the grant agreement, or confirmation from the equity administrator.

Stock Options After You Resign: Where Deadlines Hit Fast

Options aren’t RSUs. Options give you the right to buy shares at a strike price, and that right often comes with a clock after you leave. This is the “90-day trap”: People assume they have a year (or “plenty of time”), then learn the post-termination exercise window is short. Miss the window and you can lose the ability to exercise even the options that were already vested.

If you want to handle stock options resignation correctly, you’re managing three practical risks: (1) not knowing your exercise deadline, (2) not knowing the steps required to exercise, and (3) losing access to the portal or contacts you need once your employee accounts shut off. Before you resign, confirm your vested option count, the exact exercise deadline after separation, and the “how” (online portal, paper forms, wires, broker process, and who to contact when you’re no longer on internal email).

Bonus and Commission Timing: The Rule Is Usually in Writing (and Usually Strict)

Bonuses and commissions cause a different kind of regret because they feel earned. You already did the work, you already hit the numbers, and you can practically taste the payout. But many plans pay based on status on a specific date: employed on payout date, employed through the end of the quarter, or not in any ineligible status category. If you resign before that date – even with perfect performance – you may lose eligibility.

The fix is boring and effective: pull your offer letter, compensation plan, and commission policy and look for two lines. First, the eligibility rule. Second, the payout date. If either line is unclear, ask for clarification before you resign. The goal isn’t to argue – it’s to avoid the “I assumed” tax.

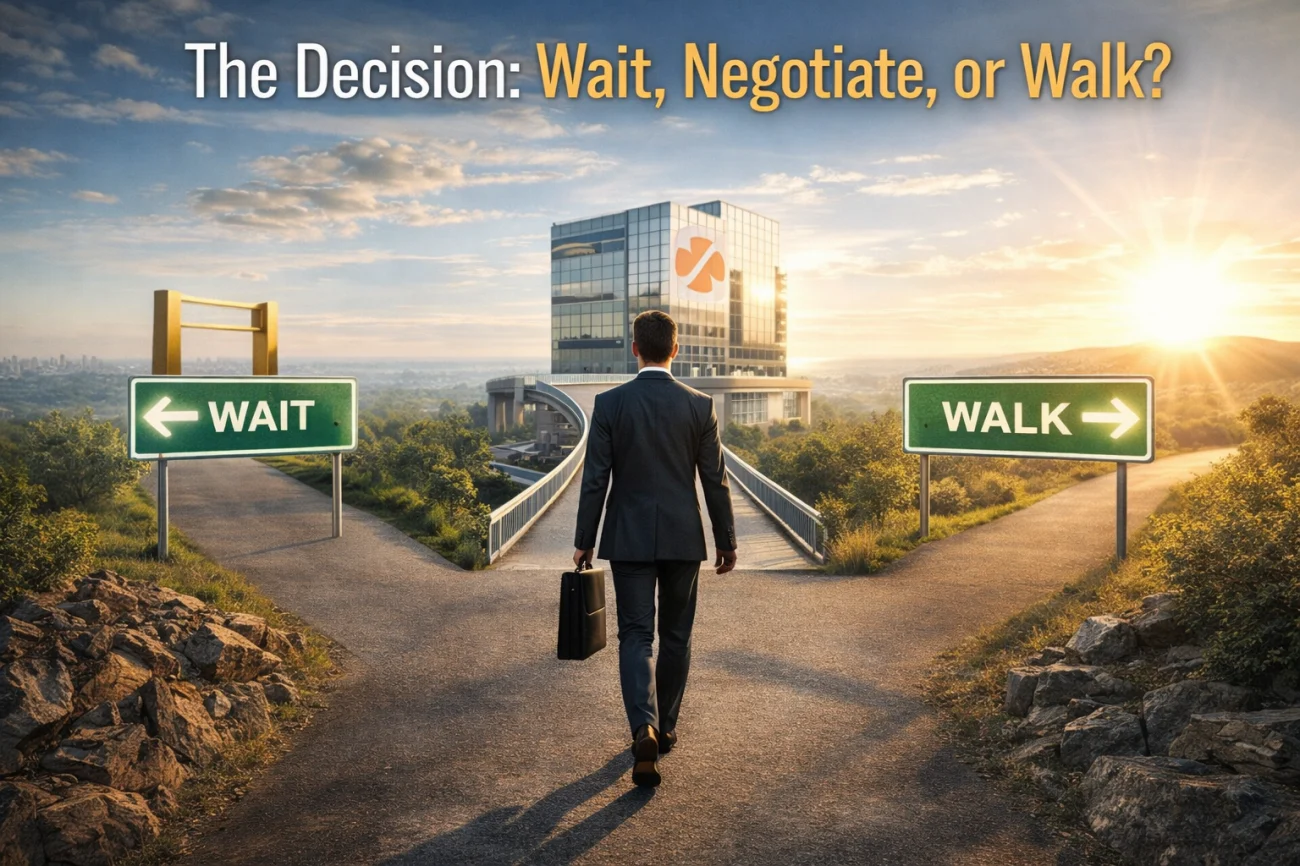

The Clean Decision Framework: Wait, Negotiate, or Walk

Once you’ve mapped the dates, the decision usually falls into one of three buckets. Waiting can be rational if a milestone is close and the value is meaningful. Negotiating can be smart if you’re forfeiting something material and you’re moving to a new role. Walking now can still be right if the personal or professional cost of staying is higher than the money – just make it a deliberate choice you won’t second-guess later.

- Wait until a vesting milestone hits (cliff date, quarterly RSU vest, bonus payout)

- Negotiate your next offer to offset what you’re forfeiting

- Walk now because staying costs more than the money

One note that helps people stop spiraling: the worst feeling isn’t “I left money.” It’s “I left money and I never knew the number.” If you’re worried about losing unvested shares, quantify it before you decide. Write down the unvested share count, the next two vest dates, and a conservative value range. You’re not predicting the stock price – you’re deciding whether timing is meaningfully expensive.

Two Neutral Emails You Can Send Before You Resign

These are designed to sound normal. You’re not announcing anything. You’re documenting compensation details “for your records,” which is a common request even for employees who are staying.

Email 1: Confirm Vesting Dates and Eligibility

Subject: Confirmation of vesting dates and eligibility

Hi [Name],

I’m reviewing my compensation details and want to confirm a few items for my records. Could you please confirm (1) my next vesting date(s) and amounts, and (2) what qualifies as being “actively employed” on a vesting date?

If there’s a plan document or portal page I should reference, feel free to point me to it as well.

Thank you,

[Your Name]

Email 2: Confirm the Post-Termination Stock Option Exercise Window

Subject: Stock option exercise window confirmation

Hi [Name],

Could you confirm the post-termination exercise period for my vested stock options and any steps required to exercise after my last day? I’d also appreciate confirmation of the number of vested options currently available to exercise.

Thanks,

[Your Name]

The 48-Hour Checklist Before You Click “Send”

If you only do one thing, do this inventory before you submit a resignation. The goal isn’t perfection – it’s avoiding the one blind spot that turns into a painful “I was so close” moment.

| Item | What to confirm | Where to look |

|---|---|---|

| Retirement match | Vesting percentage today + next milestone date | Retirement portal / plan administrator / HR |

| RSUs / performance shares | Next two vest dates + “employed on vest date” rule | Equity portal / grant agreement / equity admin |

| Stock options | Vested option count + post-termination exercise deadline | Option agreement / equity portal / broker instructions |

| Bonus / commission | Eligibility rule + payout date if you resign | Comp plan / offer letter / payroll policy |

Leave Like a Professional, Not Like a Gambler

You can leave for the right reasons and still leave at the wrong time. That doesn’t make you naïve – it makes you human.

The goal isn’t to trap you in a job you hate; it’s to make sure your decision includes the full picture, especially the part measured in dates and deadlines.

Treat your vesting period stock options like a calendar problem, not a feeling. Confirm the rules, write down the deadlines, and then choose the exit timing you can stand behind.

❓ FAQ

✅ Should I delay my resignation just to hit a vesting date?

If the milestone is close and the value is meaningful, delaying can be rational. Make it a deliberate trade-off: compare the money to the personal and professional cost of staying a bit longer.

📅 If I resign on the vesting date, do I still receive the vest?

It depends on how your plan defines being employed on that date. Some plans require active employment through the end of the day. Confirm the exact rule in writing before you time your notice.

💼 Can a new employer cover what I’m forfeiting?

Sometimes. Companies may bridge the gap with a sign-on bonus, extra equity, or an adjusted package. The more clearly you can quantify what you’re leaving behind, the easier it is to negotiate.

🧾 What’s the biggest mistake people make with stock options after leaving?

Assuming they have plenty of time. Many plans have a short post-termination exercise window, and portal access can disappear fast. Find your actual deadline, confirm the process, and decide early whether exercising is financially worth it.

🔒 Is it safe to ask HR about vesting before I resign?

Yes, if you keep it neutral and framed as documentation for your records. People ask about benefits and compensation details all the time. Use short, professional language and avoid sharing future plans.

⚠️ Legal Disclaimer: The resignation templates, email samples, and professional guidance provided in this guide are for informational purposes only and do not constitute legal advice. Employment laws and contract requirements vary by jurisdiction and individual circumstances. Please review your employment agreement and consult your HR department and/or a qualified attorney to ensure compliance with applicable laws and policies.